March Real Estate Roundup: Barry Habib Economic Forecast Webinar: A Recap

If you missed Barry Habib’s 2025 Economic Forecast webinar earlier this month, it was a great session of reflection, predictions and encouragement. Want to see it for yourself? Watch it here.

In the meantime, we’ve got some highlights below.

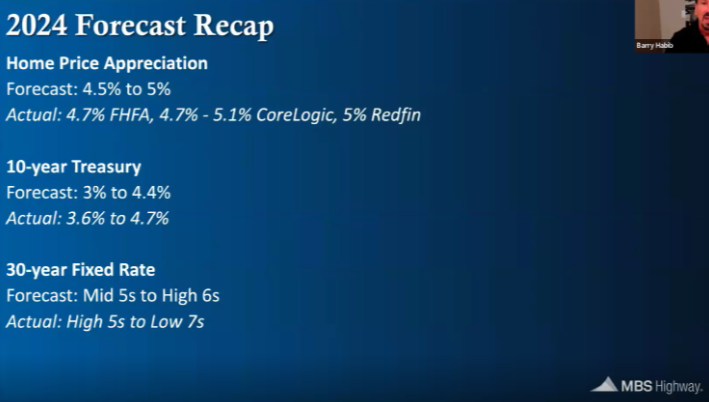

Home Price Appreciation

We’ve got to hand it to Barry, his forecast for home price appreciation was spot on.

Last year we thought home price appreciation would be 4.5 to 5%. So many people thought we were crazy because if you remember, we were coming up 8% mortgage rates, affordability was terrible. The stock market was not doing well. Most experts forecasted a decline in home prices. I remember debating it with some of the smartest minds out there. Most people thought if anything it would be flat at best on housing. But by pretty much any metric you look at, we hit a bullseye.

Interest Rates

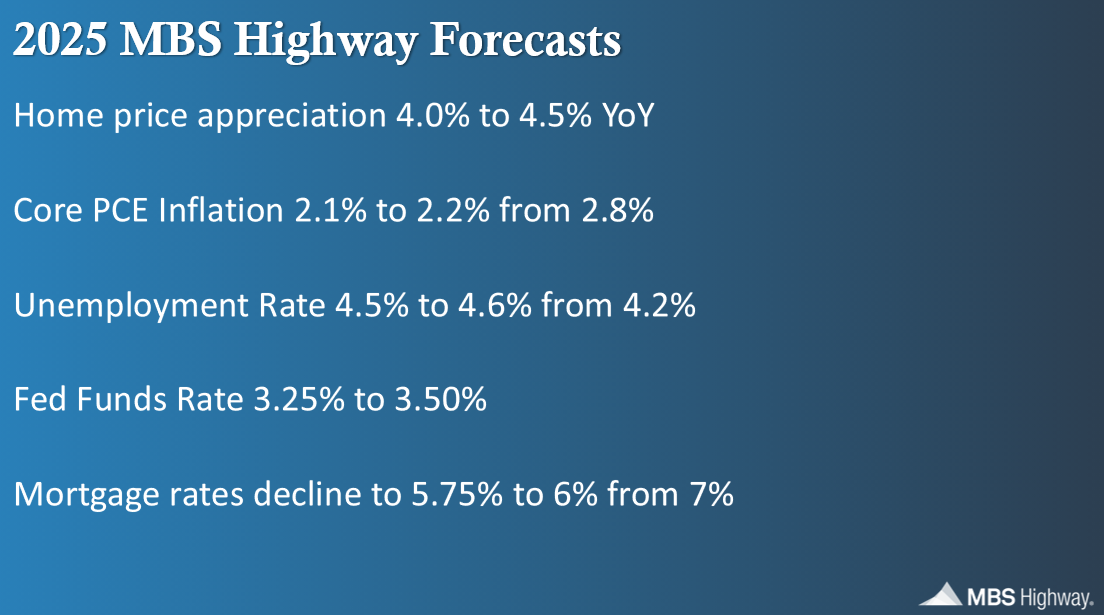

Most experts now believe that interest rates will fluctuate around the low-to-mid 6s at least through 2026. Barry suggests 5.75% is possible. A big reason is the job market.

Part of interest rates being higher than we hoped had to do with job numbers in the employment reports coming out on average a little over 200,000 jobs a month created. And the bond market didn't like that. The Fed was worried about that.

But then when they reconciled the numbers, unfortunately just a little too late, they found out that half of those jobs were not correct. I bet you if those numbers were initially reported, interest rates would have behaved a little bit better and probably either out or close to our targets.

Now, when interest rates did hit those low levels for brief periods of time around 6%, it also taught us that we don't need 4% mortgage rates. Heck, we don't even need 5% mortgage rates. It seems that a magic number for both refinances and purchase activity is around 6%. So, we've already begun a little bit of a improvement and now mortgage rates somewhere in the mid 6s to six and three quarters kind of range. But I think there's a good chance that we can get lower towards that magic level of around 6% that will help to truly unfreeze the housing market and create a lot of refinance activity too.

More on Jobs

The Wall Street Journal said one in five job postings are fake, which just tells us, again, from an economic point of view, that maybe there's more weakness in the job market. And that's a very important factor. I think the unemployment rate, which is currently at 4.1, can get up to 4.4. And that becomes a real important number. The Fed is really looking at two things, inflation and jobs. And they watch that unemployment rate and they are very careful about it.

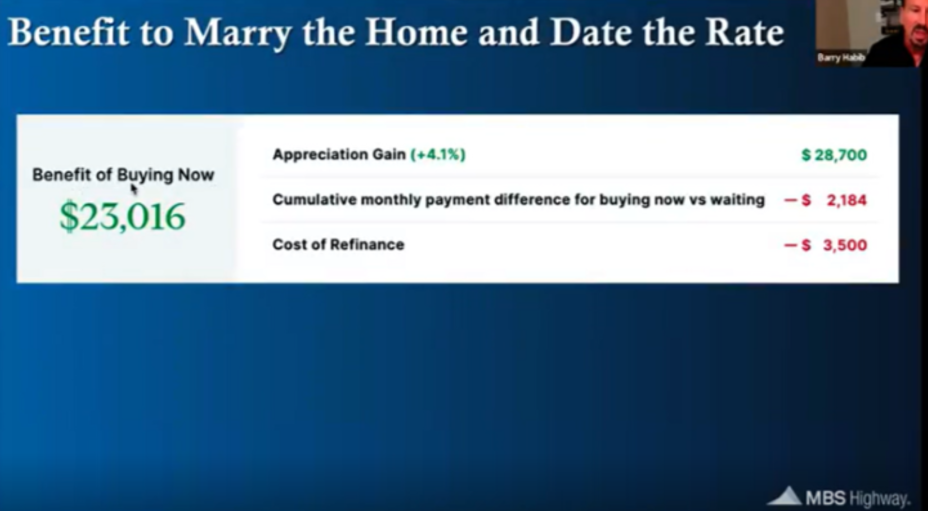

Date the Rate, Marry the Home

We’ve heard from Barry about this before - seeing the rate as a temporary means for gaining a longtime return on a home. Buying now can benefit your clients because even if rates are higher than we’d like, appreciation and refinancing are on their side.

Quick example, $700,000 home, 20% down, rate 6.875%. That is going to be a payment of $5,075 bucks a month. If they waited a year, then with appreciation, the home price would go up. If they bought today, they'd actually be paying $182 a month more. But if interest rates went down a year from now, that's $2,200, plus the cost to refinance of $3,500 to get the lower rate a year from now. It's going to cost them almost $6,000.

But what they would miss out on if they waited a year is that 4.1% appreciation, which is $28,000. See if you take the $28,000 gain minus the $6,000 cost, the reason you marry the home and date the rate is because it benefits you by $23,000.

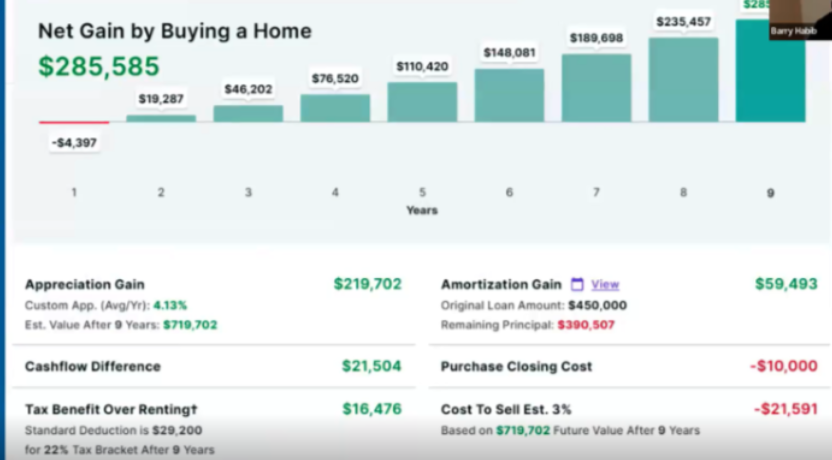

Buying Vs. Renting�

As we all know, buying is better than renting to grow long-term security.

Let's take a simple example in the Virginia Beach market, $500,000 home, 10% down, 6.5% rate…and they think they’ll be in the home for nine years. Let’s say rent is about $3,600 a month, and new rents are going up at 5%. Historical appreciation for the last 63 years has been 4.2% in this market. So, we could see that by buying, you're more expensive than renting.

But that changes. This is year one. The fifth year, your rent is more expensive than buying. Plus, you’re paying principal when you buy. Principal is not a cost; it's your own money. If you took all of the rent that you'd spend over the nine years, and if you took all of the money you'd spend buying, you'd be better off by $21,000 buying compared to renting. And with the principal portion of this, you gain about $5,000 plus every year, and by the ninth year you've gained almost $60,000 in principal.

Why? Because you started off with a $450k mortgage, and nine years later your balance is only $390k. So, you started with a $50,000 down payment. That was your equity. Here you have $110,000 in equity plus the magic of appreciation. At just 4.1% appreciation, would it surprise you that that's an extra $220,000? So, the $60k plus the $220k plus your tax benefit that you get over renting.

Now let's subtract the cost to sell. And the reason why you want to buy versus renting is it's $285,000 better over the nine years. Now look, if you're going to move within a year, you should rent because you'd lose money by buying. But if you're going to be there two years or longer, why in the world would you not be buying this home?

Be in the Wisdom Business

A few parting thoughts from Barry on how to talk to your clients this year:

If you go into a clothing store and the salesperson, no matter what you try on, no matter how horrendous it might look, says “Oh my gosh, that's fantastic!” This is someone that is not gaining your trust. You will trust the person who says, “I wouldn't get that.”

Of course we should be positive, it’s what we do. But you should also try and find things that actually put you in a position of being their advocate where you could say, hey, here's something that you should know. You’ll need a new roof, or the driveway is going to need some patches. They feel like you're their advocate.

Now, the other way to gain trust is with market expertise. I think this starts with understanding what type of business you want to be in. Do you want to be in the information business, or do you want to be in the wisdom business? Anyone can google information. Wisdom you tend to pay for. When you go to a doctor, that's wisdom. When you go to an attorney, that's wisdom. Because people pay for wisdom. They don't expect to pay for information.

We hope Barry’s forecast has provided a solid roadmap for you this year. Call with any questions!